Our latest commercial real estate update provides a snapshot of the Australian CBD office leasing markets. We base our insights on the latest market data and our experience on the ground.

Sydney’s overall vacancy rate sits at 13.7% as at July 2025, the highest level since the early 1990s and a clear sign that new supply is still running ahead of demand. The picture by grade is quite mixed. A Grade vacancy climbed to 17.6% (from 15.2% in January), and B Grade has moved up to 14.4% (from 12.9%), showing continued softness in secondary assets. In contrast, Premium vacancy has tightened to 9.8% (from 10.9%), reflecting tenants’ preference toward the top tier buildings despite broader softness.

Vacancy is also unfolding differently across the CBD. In the Core, Premium space is relatively tight at 8.8%, while A Grade sits at 15.0% and B Grade at 15.8%. Outside the Core, including the Western Corridor, Southern and Midtown precincts – vacancies are generally in the mid-teens, highlighting softer demand and more choice for tenants in these fringe CBD locations.

Around 73,000 sqm of new and refurbished stock came to market in H1 2025, including

A further 28,300 sqm is due in H2 2025 from the refurbishments of 270 Pitt Street (23,000 sqm) and 1 Kent Street (5,300 sqm) into future A-Grade assets. Neither has pre-commitments at this stage, so they represent the main source of fresh, uncommitted space in this cycle.

The next substantial supply wave is not until 2027, when more than 170,000 sqm is scheduled at 55 Pitt Street (63,000 sqm, ~35% pre-committed), Atlassian HQ (57,000 sqm, fully pre-committed) and Chifley Tower South (53,000 sqm, ~50% pre-committed). Beyond this, the pipeline is expected to slow as higher construction costs and limited pre-leasing make new projects harder to commence.

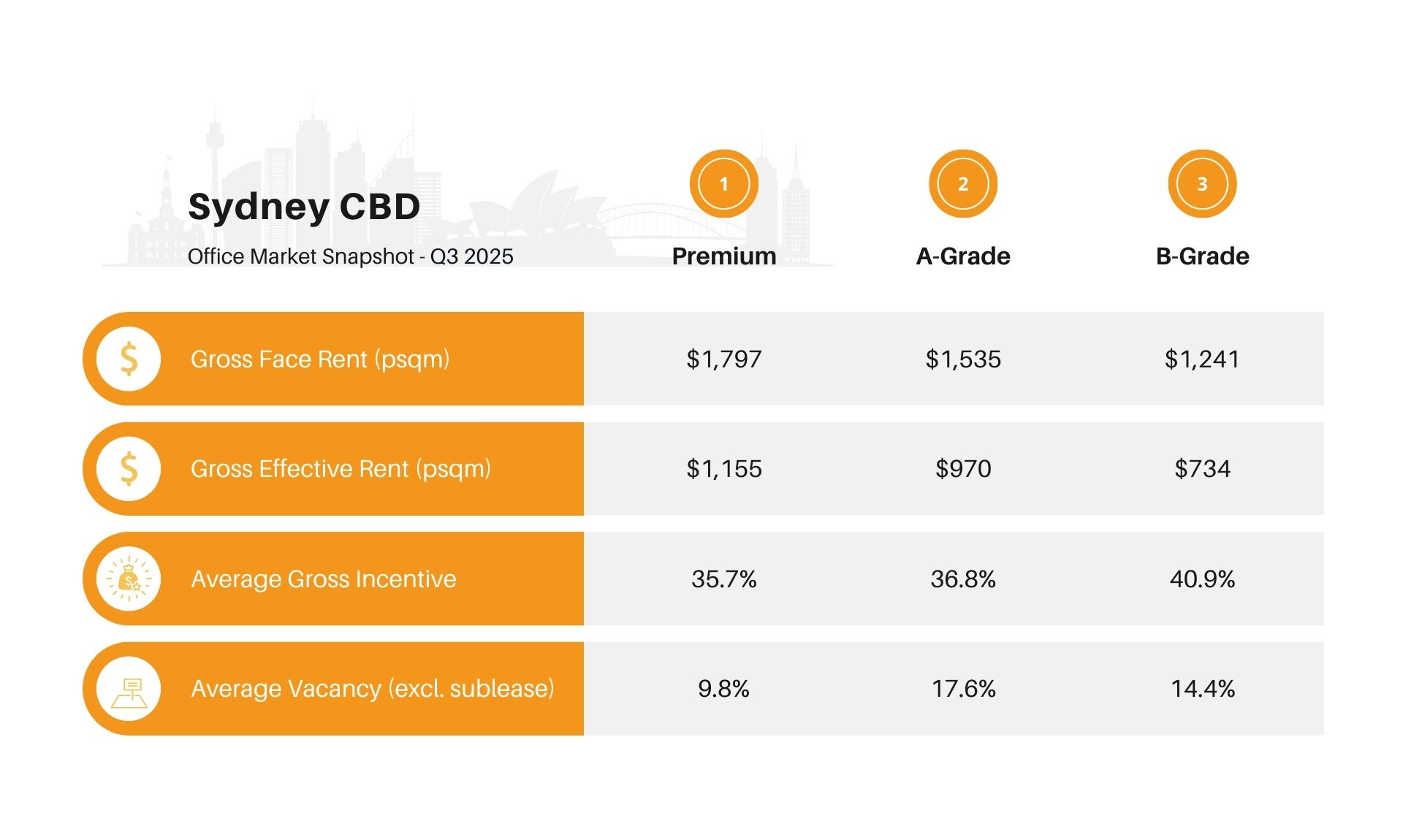

Face rents moved higher at the top end of the market in Q3 2025. Premium increased 3.0% quarter-on-quarter to $1,797 sqm (+5.6% YoY) and A Grade rose 3.0% to $1,535 sqm (+2.8% YoY). In contrast, B Grade face rents fell 5.0% over the quarter to $1,241sqm, although they remain 5.3% higher than a year ago, reflecting ongoing repricing of older stock.

Effective rents edged up slightly. Premium gross effective rents rose 0.3% to $1,155/sqm (7.9% YoY), A Grade increased 1.8% to $970/sqm, and B Grade lifted 0.7% to $734/sqm, still slightly below levels a year ago. Incentives were stable in Premium at 35.7% and eased marginally in A Grade to 36.8%, while B Grade incentives increased to 40.9%. For tenants, this translates to firmer pricing in Premium and A Grade, but continued negotiating power in secondary assets where landlords are relying more heavily on incentives to secure deals.

Sublease availability in the Sydney CBD has stabilised through the first half of 2025 and is now below the historical average. As of June, sublease space accounted for 0.8% of total stock, or 42,940 sqm. Availability is still dominated by financial services, tech, and professional firms. Notable tranches include:

With growing diversity and motivated landlords, sublease space offers tenants a chance to secure prime locations at competitive rates.

Demand remains elevated for high-quality space in the Sydney CBD Core, particularly upper floors of Premium buildings, driven by proximity to public transport, key amenities, and city views, with active enquiry now over 400,000 sqm, the highest level since 2014. In contrast, more cost-sensitive occupiers are increasingly exploring peripheral markets such as the Western Corridor, Southern precinct, and Midtown, where higher vacancy and softer rents provide meaningful discounts to Core Premium space.

Some of the recent notable commitments shaping the Sydney CBD market include:

Australia’s tech sector continues to scale, with around 40,000 tech companies, more than 1 million jobs and tech spending projected to grow 8.7% YoY, outpacing the broader APAC region. Within Sydney, this growth is increasingly concentrating in Tech Central, anchored by Atlassian.

Central, Central Place and the Post House, which together will deliver over 200,000 sqm of new-generation office space targeted at technology and innovation tenants. Atlassian Central alone is a 39-storey, 59,100 sqm Premium tower designed as one of the world’s tallest hybrid-timber office buildings, with an electricity-generating façade, and a fully electric, targeting market-leading Green Star and NABERS Energy ratings. When complete, Atlassian is expected to offer around 21,000 sqm for sublease across four floors in three pods, creating a rare opportunity for other occupiers to access brand-new, ESG-led space within a flagship HQ building. The Sydney Start-up Hub’s relocation from York Street into the Tech Central precinct at Pitt Street will pull early-stage and scale-up businesses into the same neighbourhood as larger tech corporates, deepening the cluster effect around Central Station. For clients wanting a deeper dive on the numbers, pipeline and tenant mix in Tech Central, we can share our 2025 Tech Deck or you can reach out to our Director, Francois Rollin, for a more detailed discussion.

Size requirements are beginning to stabilise as hybrid workplace models mature and businesses become clearer on how they want people to use the office. Organisations are testing a range of approaches, from anchor days to activity-based and team-led models – but, importantly, most now have a better handle on typical attendance patterns and space needs than they did two or three years ago. This is consistent with what our team, including Associate Director Courtney Magro, is seeing in recent tenant projects, where requirements are being framed with greater confidence around long-term workplace intent rather than short-term experimentation.

The sharp space give-backs of the immediate post-Covid period have eased, and this is now showing up in the sublease market: availability has fallen back below the 10-year average, indicating fewer tenants are carrying large amounts of excess space. Against this backdrop of more right-sized footprints, elevated construction costs and the highest CBD vacancy in around three decades, fewer landlords are willing to deliver full whole-floor speculative fitouts. Instead, they are focusing on lighter refurbishments or smaller suite-style spec, with layouts and capex more closely aligned to increasingly specific, data-driven tenant briefs.

You may have seen the headlines: new office developments in Sydney CBD are drying up, with no new buildings expected in 2026 and only a few slated for 2027. Some are calling it a turning point suggesting that the market is tightening, and tenants should brace for rising rents and shrinking incentives. But is this really the end of tenant-friendly conditions in Sydney’s CBD? Not quite. While this trend may apply to premium-grade assets in the Core CBD, it’s only part of the picture. As François Rollin, Sydney Director, explains:

“Pre-commitments are falling short, especially for larger size requirements. Vacancy rates in Sydney CBD have reached their highest levels since the early 1990s for both A and B grade assets. And with AI reshaping workforce needs, there’s a layer of uncertainty around future office demand.”

Beyond the CBD, the story continues. Just minutes away via Metro, vacancy rates remain high in key suburban markets (23,7% in North Sydney, 30,5% in St Leonards, 17,7% in Chatswood and 18,9% in Macquarie Park) making it great alternatives for tenants looking for more cost-effective solutions.

Sydney’s legal district is gradually shifting away from the traditional court precinct as leading law firms relocate to the newly revamped AMP Building at 33 Alfred Street in Circular Quay. This emerging hub will prominently feature Allens, occupying the top nine floors, alongside other major firms such as Lander & Rogers, Maddocks and Pinsent Masons. The movement reflects a broader trend of law firms seeking to upgrade their office space to strengthen corporate image, attract and retain talent, and support a return to in-office work. Recent relocations of Johnson Winter Slattery and Corrs to Quay Quarter Tower, and Gadens to Chifley Square, underline a clear preference for premium, well-located offices that combine prestige, amenity and transport connectivity.

A recent Tenant CS study of 75 mid- and top-tier law firms in Sydney found that around 39% had downsized, 60% had upsized, and the average tenure in a single building was approximately 7.5 years, driven by high relocation and fitout costs. For legal occupiers, these long commitments place a premium on getting building quality, flexibility and location right at the outset, as today’s decisions will frame workplace and brand outcomes over much of the next decade.

Sustainability is now a core filter for office occupiers, particularly larger corporates with formal decarbonisation targets. Tenant CS Director Hamish Mackay notes that for many local and offshore tenants, strong ESG credentials are treated as a baseline requirement, not a “nice to have”

Tenants are gravitating towards higher-grade assets with strong Green Star, NABERS and/or WELL ratings. At the same time, recent analysis indicates only around 28% of Australian office buildings are on track to meet major tenants’ climate needs, highlighting how limited the pool of genuinely future-proof assets still is. This is widening the gap between newly built or comprehensively refurbished towers and older, more carbon-intensive stock.

The future Atlassian HQ at Tech Central (due 2027) illustrates where demand is heading: a low-carbon, hybrid-timber, fully electric building targeting leading sustainability ratings. For tech and innovation-led occupiers, assets of this type align leasing decisions with climate commitments and employee expectations, while reducing exposure to future regulatory and carbon-cost risk.

Melbourne CBD vacancy remains elevated at 17.9% as at Q2 2025. By grade, vacancy is 16.4% in Premium, 19.3% in A Grade and 18.9% in B Grade, keeping conditions firmly in tenants’ favour. At a precinct level, the Eastern Core (13.8%) and North Eastern (13.0%) are the tightest sub-markets, while Spencer (21.9%) and Flagstaff (20.6%) continue to show the deepest vacancy and therefore the strongest leverage for occupiers open to western CBD locations.

Q3 saw completion of the 85 Spring Street refurbishment (~12,000 sqm, ~80% pre-committed), the first major delivery of 2025. This adds a modest amount of prime space and triggers further backfill as tenants upgrade from older buildings. The next substantial wave of new stock is now concentrated in 2026, with the scheduled completion of 17 Bennetts Lane (~12,000 sqm), 7–23 Spencer Street (~46,000 sqm, <10% pre-committed), 51 Flinders Lane (~29,000 sqm, largely pre-committed to WPP), 435 Bourke Street (60,000+ sqm, ~26% pre-committed to CBA) and Town Hall Place (~17,000 sqm, majority pre-committed).

With vacancy still elevated, leasing conditions are likely to remain favourable for tenants over the long term, especially for larger occupiers and those open to secondary locations or backfill space.

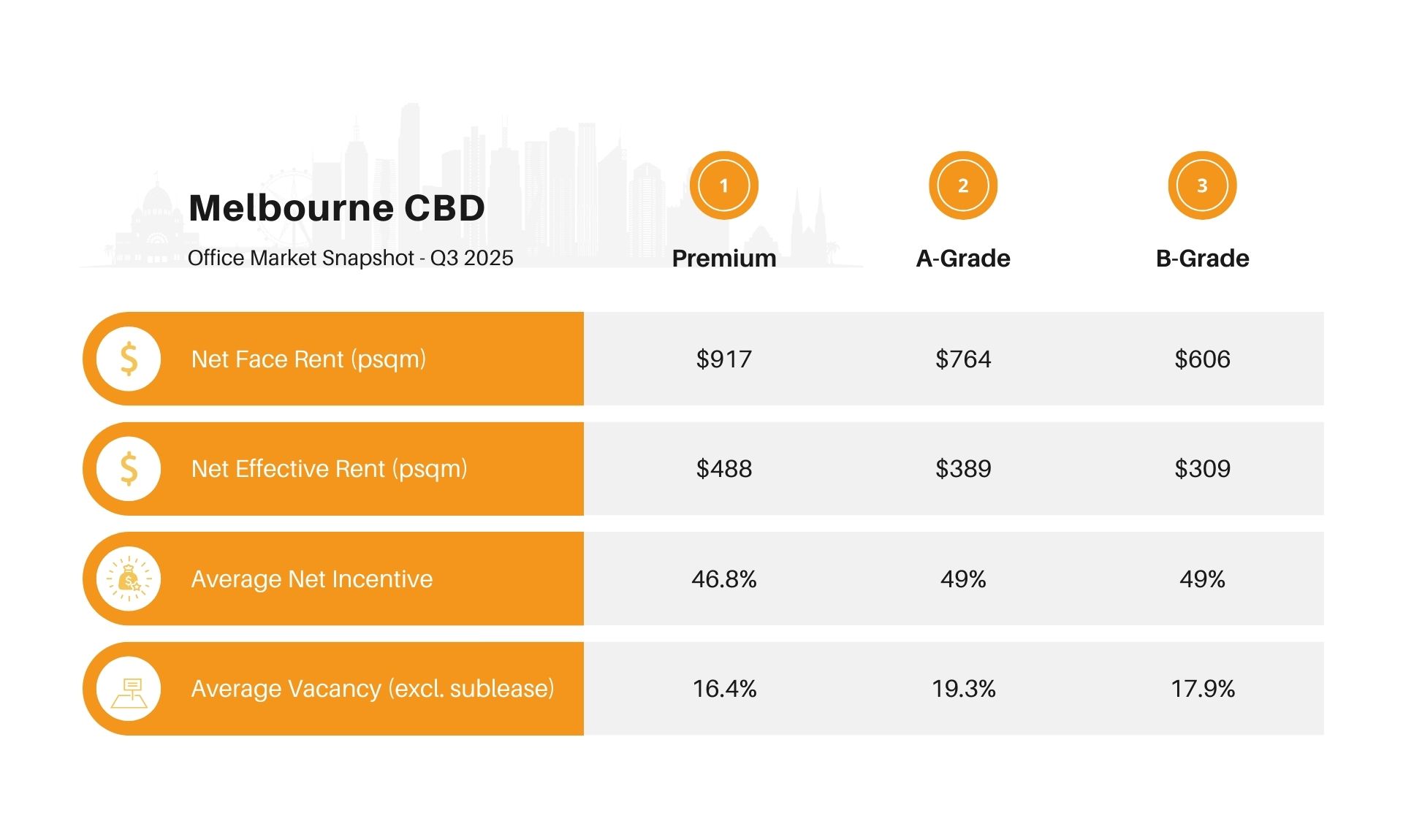

In Q3 2025, Melbourne CBD face rents moved higher again across all grades, while incentives remained elevated. Premium net face rents rose 5.9% QoQ to $917/sqm, A Grade increased 5.2% to $764/sqm, and B Grade lifted 0.7% to $606/sqm. On a year-on-year basis, Premium and A Grade face rents are now up 12.5% and 6.4% respectively, while B Grade is 3.8% lower than a year ago.

The impact on effective rent is more muted. Premium effective rents increased 5.9% QoQ to $488/sqm, A Grade rose 5.1% QoQ to $389/sqm and B Grade edged up 0.7% QoQ to $309/sqm, still around 3.4% below Q3 2024. Incentives remain high at around 46.8% in Premium and 49% in A and B Grade, with only B Grade changing this quarter (-0.6%)

The longer-term picture is that face rents have grown, but effective rents have more muted growth. Since 2018, Premium effective rents have slipped from $495/sqm to $488/sqm, A Grade from $405/sqm to $389/sqm and B Grade from $320/sqm to $309/sqm, despite steady headline rent growth. For tenants, leasing conditions remain favourable: high incentives and elevated vacancy continue to contain net effective rents, particularly in A and B Grade stock, where there is still good scope to secure competitive packages on both new and renewal deals.

Melbourne CBD sublease vacancy is now sitting at around 1.2% of stock (62,143 sqm), down from about 1.6% a year earlier and below its long-term average. Most precincts are now under 2%, with the North Eastern precinct still recording the highest level of sublease space.

Despite the decline, Melbourne still records the highest sublease availability of any Australian capital. For tenants, subleasing remains attractive given its lower effective rents, fitted layouts, and shorter terms, offering cost and flexibility advantages over direct lease options.

Melbourne CBD recorded its first period of positive net absorption since 2022, standing at +1,446 sqm in H1 2025. Growth was led by Grade B and Premium, partly offset by continued weakness in A Grade. At a precinct level, the Eastern Core and Western Core outperformed, while Docklands and the North Eastern precinct recorded further negative absorption.

Although the headline shift into positive territory signals a marginal improvement, demand remains well below historical norms. Elevated vacancy and generous incentives ensure occupiers continue to hold strong negotiating power.

Some of the commitments which will shape the future of the Melbourne CBD include:

Our observation of stronger B Grade take-up has been confirmed in H1 2025 with PCA’s biannual report released in August. Melbourne CBD recorded overall net absorption of +1,446 sqm, with Grade B contributing +15,031 sqm, the standout performer across all grades. This uplift reflects tenants relocating from suburban and fringe markets into more central locations, suggesting that for many occupiers, CBD positioning is taking precedence over building quality.

This contrasts with other capitals where the “flight to quality” has dominated. In Melbourne, Premium absorption was positive but more modest (+4,520 sqm), while A Grade contracted. The data indicates tenants are prioritising affordability and location over quality upgrades, softening the flight-to-quality narrative in this market.

From 1 January 2026, the Melbourne congestion levy on off-street parking will rise sharply, with Category 1 (CBD) increasing from $1,750 to $3,030 per bay per year and Category 2 (inner fringe) rising from $1,240 to $2,150 per bay per year – lifts of roughly 70%. The Category 2 levy area will also expand to include parts of Burnley, Cremorne, Richmond, Abbotsford, South Yarra, Windsor and Prahran, as well as sections along St Kilda Road, while the Queen Victoria Market area moves to the lower Category 2 rate.

The impact will be most pronounced for tenants with large parking allocations, where the levy is typically passed through via outgoings or licence fees and can materially increase total occupancy costs even if office rents remain steady. Several fringe and city-edge precincts that were previously relatively low-cost for parking will now carry a much higher levy. As a result, the congestion levy will become a more important factor for companies with high parking requirements when assessing which suburbs and buildings to target in the next lease cycle, sitting alongside rent, incentives, transport access and staff catchments in occupier decision-making.

Fitted space continues to be leased ahead of vacant space, but in the sub-300sqm market there is now a clearer hierarchy emerging. Well-designed, modern spec suites are being leased noticeably faster than older or more generic specs, as smaller tenants prioritise quality, convenience and avoiding upfront fitout spend. Older spec fitouts are still leasing, but typically require sharper incentives or some landlord contribution towards refresh works to compete with newer, better-presented options.

In Melbourne, ESG credentials remain an important consideration, with tenants continuing to prefer buildings that offer strong NABERS ratings and sustainability initiatives. However, these buildings typically sit in the Premium and A Grade market, where demand has weakened. A Grade recorded the largest contraction in H1 2025, while B Grade was the only segment to show meaningful positive absorption. This pattern highlights that for many occupiers, affordability and location are outweighing ESG aspirations. Cost-conscious tenants are gravitating toward B Grade stock, even as premium assets hold their environmental advantage. With face and effective rents in secondary stock under pressure, cost remains the dominant driver of leasing decisions, while ESG is increasingly seen as a “nice to have” rather than a “must have”.

Brisbane CBD vacancy remains at 10.7%, consistent with the latest PCA bi-annual report. Premium vacancy is unchanged at 3.8%, while A Grade and B Grade also hold at 9.6% and 14.9%, reinforcing the continued split between tight Premium availability and softer mid-tier conditions.

On the supply side, 205 North Quay is now complete and fully occupied by Services Australia, with 360 Queen Street (~45,000 sqm) set to be the next major addition. The tower is due in late 2025 and is now close to 90% pre-committed, led by BDO, Herbert Smith Freehills and other large occupiers. Beyond this, committed future supply remains limited, with the 450 Queen Street refurbishment (~17,500 sqm, 2026) and Waterfront Brisbane North Tower (~72,000 sqm, 2028, ~50% pre-committed) forming the next wave of new stock. Other mooted projects, including 101 Albert Street and 60 Queen Street, remain uncommitted and are unlikely to reach the market before 2028.

With Premium vacancy already tight and limited new space coming online, competition for high-quality buildings remains elevated. In contrast, A and B Grade vacancy is stable but high, offering tenants broader choice, stronger incentives and greater negotiation leverage in the mid-tier.

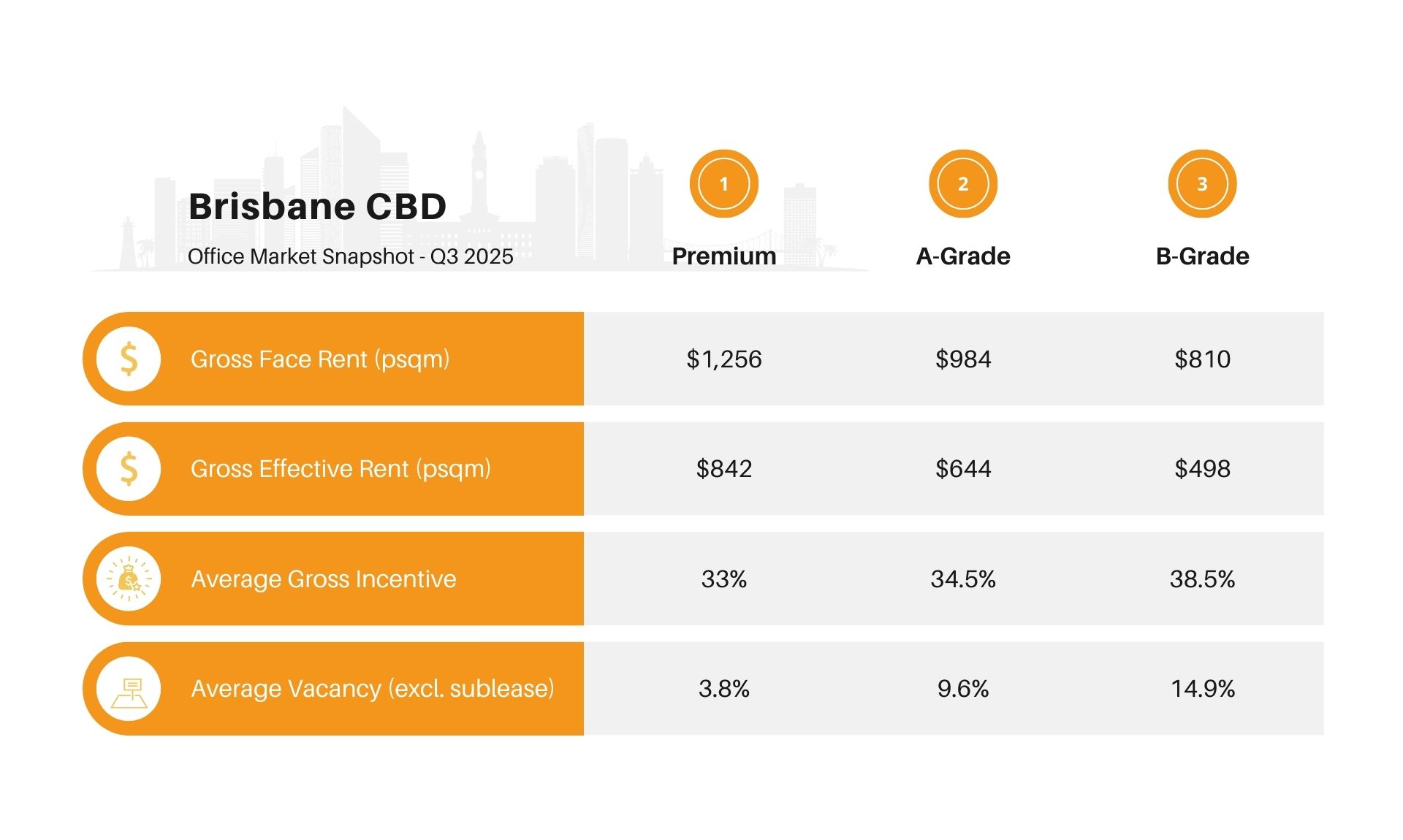

Gross face rents increased again in Q3 2025, with Premium rising to $1,256/sqm, A Grade to $984/sqm, and B Grade to $810/sqm. Growth was strongest in A Grade (5.0% QoQ), followed by Premium (3.7%) and B Grade (2.5%). On an annual basis, rents have lifted between 11–14%, reflecting ongoing upward pressure despite mixed demand conditions.

Incentives edged lower across all grades, now sitting at 33% in Premium, 34.5% in A Grade, and 38.5% in B Grade. The reduction is modest but continues the trend of tightening terms in higher-quality assets as Premium supply remains constrained and stronger A Grade options absorb enquiry.

These movements pushed effective rents higher again this quarter. Premium rose 5.3% QoQ, A Grade lifted 6.6%, and B Grade increased 4.2%. The strongest momentum remains in A Grade, where falling incentives are amplifying rental growth despite vacancy holding at 9.6%. B Grade continues to offer the most favourable terms for tenants, with incentives near 40% softening the impact of rising face rents.

Brisbane CBD sublease vacancy was recorded at 0.9% of total stock (~20,900 sqm) in July 2025, down from 1.2% (~27,800 sqm) in January. This places current sublease availability below the city’s long-term average of ~1.0%. Reductions of sublease vacancy can be attributed to the removal of listings, transfer of sublease to direct vacancies and uptake of the space.

Leasing activity in the Brisbane CBD remained subdued in Q2 2025, with many occupiers opting to renew rather than relocate amid cost pressures and ongoing caution. Decision-making timelines remain extended, particularly for larger corporates, contributing to a slow flow of new commitments.

Despite this softer backdrop, Brisbane recorded the strongest net absorption of any CBD in the first half of 2025, reflecting a handful of large occupier moves rather than broad-based demand. This strength was concentrated in Premium assets as we noted vacancy tightened to 3.8%

Notable tenant movements in Q3 2025 shaping Brisbane CBD include:

Brisbane now ranks as the most expensive city to build in Australia, with average construction costs hitting approximately $5,009 psqm, edging ahead of Sydney and Melbourne. Pressure is mounting: Arcadis reports a 5.2% cost escalation in 2024, with a further 5% projected for 2025, and a staggering 30.5% cumulative cost rise expected by 2029, driven by Olympic-related demand, acute labour shortages, and wage inflation. The labour market is stretched estimates suggest a shortfall of 41,000 skilled workers across Queensland, exacerbating delays and escalating budgets.

At the same time, government infrastructure programs (notably 2032 Games preparations and Cross River Rail) are siphoning off capacity and labour from commercial projects, further squeezing new office developments. Adding to these pressures is poor labour productivity on major projects. Industry leaders warn that union-backed rostering is leaving some sites effectively operating at only two to three productive days per week, even as wages climb. Treasury modelling suggests this could lift project costs by up to 25% by 2030, highlighting systemic inefficiencies that make new office towers harder and slower to deliver. These conditions are a double-edged sword, on one hand, the difficulty and cost of delivering new high-quality towers gives landlords reason to hold firm on pre-commitment pricing and tighten incentives. On the other, there’s growing opportunity in existing A and B Grade buildings, where owners are investing in sustainability and productivity upgrades to remain competitive and leveraging incentives to attract occupiers.

Brisbane’s flight-to-quality continues to accelerate as organisations compete for talent and reinforce in-office attendance. With only eight Premium buildings in the entire CBD, high-quality space is structurally scarce, and demand is concentrating heavily at the top end of the market. In Q2 2025, Premium vacancy fell sharply from 7.3% to just 3.8%, its lowest level in more than four years, underscoring how quickly new or refurbished space is absorbed once it becomes available. By contrast, vacancy increased in A Grade (to 9.6%) and B Grade (to 14.9%) as occupiers either traded up or sought better amenity without paying Premium rents. The divergence shows that while overall CBD vacancy edged up to 10.7%, genuine high-quality options are shrinking. For tenants targeting Premium towers, early engagement is becoming essential. Those prepared to consider upgraded A or B Grade assets will benefit from broader choice, stronger incentives, and materially better negotiating leverage.

New CBD towers are thin on the ground over the next few years, with only a small number of committed projects adding to the total office pool and much of that space already pre-leased. From here, most leasing options will come from churn and backfill as tenants move into new or refurbished buildings, rather than from large volumes of brand-new stock. At the same time, some older secondary assets are being withdrawn or converted to other uses, meaning the market is gradually reshaping more than expanding. For tenants, the practical outcome is a market where the best value is increasingly found in existing A and better B Grade buildings, particularly refurbished or partially upgraded assets - offering a mix of established locations, improved services and negotiable commercial terms.

Brisbane’s fringe office market is heating up as more businesses look beyond the CBD for workspace. With rising rents and tighter availability in the city centre, companies are increasingly turning to fringe areas like Fortitude Valley, South Brisbane, and Newstead for more affordable, high-quality office spaces. According to the PCA, the fringe recorded a 10.5% vacancy, which has been on the decline for a number of years.

This shift is being driven by vacancy rates tightening and limited new supply, Brisbane’s fringe office market is proving to be an attractive alternative for companies looking to expand or relocate.

In most Australian cities it’s a tenant’s market and will be for the foreseeable future. Landlords are competing to secure quality occupants on long leases and are more flexible than they have been in years.

Opportunistic tenants are taking advantage of favourable market conditions by renegotiating terms in their existing space or relocating to a better building.

To secure the best terms, tenants need only find the soft spots in the market and develop their strategy around landlord motivators.

But the landscape is challenging to navigate alone. Even in a favourable market, there's more to negotiate, and tenants need access to the whole market to get the best deal.

Tenant CS is an independent tenant advisory firm that exclusively represents tenants in commercial negotiations to secure favourable lease terms and savings.

Book a discovery call to find out how we can help you with your next lease negotiation or relocation project.

Author

.png)

Share this article

Follow us

Our latest commercial real estate update provides a snapshot of the Australian CBD office leasing markets. We base our insights on the latest market data and our experience on the ground.

Sydney’s overall vacancy rate sits at 13.7% as at July 2025, the highest level since the early 1990s and a clear sign that new supply is still running ahead of demand. The picture by grade is quite mixed. A Grade vacancy climbed to 17.6% (from 15.2% in January), and B Grade has moved up to 14.4% (from 12.9%), showing continued softness in secondary assets. In contrast, Premium vacancy has tightened to 9.8% (from 10.9%), reflecting tenants’ preference toward the top tier buildings despite broader softness.

Vacancy is also unfolding differently across the CBD. In the Core, Premium space is relatively tight at 8.8%, while A Grade sits at 15.0% and B Grade at 15.8%. Outside the Core, including the Western Corridor, Southern and Midtown precincts – vacancies are generally in the mid-teens, highlighting softer demand and more choice for tenants in these fringe CBD locations.

Around 73,000 sqm of new and refurbished stock came to market in H1 2025, including

A further 28,300 sqm is due in H2 2025 from the refurbishments of 270 Pitt Street (23,000 sqm) and 1 Kent Street (5,300 sqm) into future A-Grade assets. Neither has pre-commitments at this stage, so they represent the main source of fresh, uncommitted space in this cycle.

The next substantial supply wave is not until 2027, when more than 170,000 sqm is scheduled at 55 Pitt Street (63,000 sqm, ~35% pre-committed), Atlassian HQ (57,000 sqm, fully pre-committed) and Chifley Tower South (53,000 sqm, ~50% pre-committed). Beyond this, the pipeline is expected to slow as higher construction costs and limited pre-leasing make new projects harder to commence.

Face rents moved higher at the top end of the market in Q3 2025. Premium increased 3.0% quarter-on-quarter to $1,797 sqm (+5.6% YoY) and A Grade rose 3.0% to $1,535 sqm (+2.8% YoY). In contrast, B Grade face rents fell 5.0% over the quarter to $1,241sqm, although they remain 5.3% higher than a year ago, reflecting ongoing repricing of older stock.

Effective rents edged up slightly. Premium gross effective rents rose 0.3% to $1,155/sqm (7.9% YoY), A Grade increased 1.8% to $970/sqm, and B Grade lifted 0.7% to $734/sqm, still slightly below levels a year ago. Incentives were stable in Premium at 35.7% and eased marginally in A Grade to 36.8%, while B Grade incentives increased to 40.9%. For tenants, this translates to firmer pricing in Premium and A Grade, but continued negotiating power in secondary assets where landlords are relying more heavily on incentives to secure deals.

Sublease availability in the Sydney CBD has stabilised through the first half of 2025 and is now below the historical average. As of June, sublease space accounted for 0.8% of total stock, or 42,940 sqm. Availability is still dominated by financial services, tech, and professional firms. Notable tranches include:

With growing diversity and motivated landlords, sublease space offers tenants a chance to secure prime locations at competitive rates.

Demand remains elevated for high-quality space in the Sydney CBD Core, particularly upper floors of Premium buildings, driven by proximity to public transport, key amenities, and city views, with active enquiry now over 400,000 sqm, the highest level since 2014. In contrast, more cost-sensitive occupiers are increasingly exploring peripheral markets such as the Western Corridor, Southern precinct, and Midtown, where higher vacancy and softer rents provide meaningful discounts to Core Premium space.

Some of the recent notable commitments shaping the Sydney CBD market include:

Australia’s tech sector continues to scale, with around 40,000 tech companies, more than 1 million jobs and tech spending projected to grow 8.7% YoY, outpacing the broader APAC region. Within Sydney, this growth is increasingly concentrating in Tech Central, anchored by Atlassian.

Central, Central Place and the Post House, which together will deliver over 200,000 sqm of new-generation office space targeted at technology and innovation tenants. Atlassian Central alone is a 39-storey, 59,100 sqm Premium tower designed as one of the world’s tallest hybrid-timber office buildings, with an electricity-generating façade, and a fully electric, targeting market-leading Green Star and NABERS Energy ratings. When complete, Atlassian is expected to offer around 21,000 sqm for sublease across four floors in three pods, creating a rare opportunity for other occupiers to access brand-new, ESG-led space within a flagship HQ building. The Sydney Start-up Hub’s relocation from York Street into the Tech Central precinct at Pitt Street will pull early-stage and scale-up businesses into the same neighbourhood as larger tech corporates, deepening the cluster effect around Central Station. For clients wanting a deeper dive on the numbers, pipeline and tenant mix in Tech Central, we can share our 2025 Tech Deck or you can reach out to our Director, Francois Rollin, for a more detailed discussion.

Size requirements are beginning to stabilise as hybrid workplace models mature and businesses become clearer on how they want people to use the office. Organisations are testing a range of approaches, from anchor days to activity-based and team-led models – but, importantly, most now have a better handle on typical attendance patterns and space needs than they did two or three years ago. This is consistent with what our team, including Associate Director Courtney Magro, is seeing in recent tenant projects, where requirements are being framed with greater confidence around long-term workplace intent rather than short-term experimentation.

The sharp space give-backs of the immediate post-Covid period have eased, and this is now showing up in the sublease market: availability has fallen back below the 10-year average, indicating fewer tenants are carrying large amounts of excess space. Against this backdrop of more right-sized footprints, elevated construction costs and the highest CBD vacancy in around three decades, fewer landlords are willing to deliver full whole-floor speculative fitouts. Instead, they are focusing on lighter refurbishments or smaller suite-style spec, with layouts and capex more closely aligned to increasingly specific, data-driven tenant briefs.

You may have seen the headlines: new office developments in Sydney CBD are drying up, with no new buildings expected in 2026 and only a few slated for 2027. Some are calling it a turning point suggesting that the market is tightening, and tenants should brace for rising rents and shrinking incentives. But is this really the end of tenant-friendly conditions in Sydney’s CBD? Not quite. While this trend may apply to premium-grade assets in the Core CBD, it’s only part of the picture. As François Rollin, Sydney Director, explains:

“Pre-commitments are falling short, especially for larger size requirements. Vacancy rates in Sydney CBD have reached their highest levels since the early 1990s for both A and B grade assets. And with AI reshaping workforce needs, there’s a layer of uncertainty around future office demand.”

Beyond the CBD, the story continues. Just minutes away via Metro, vacancy rates remain high in key suburban markets (23,7% in North Sydney, 30,5% in St Leonards, 17,7% in Chatswood and 18,9% in Macquarie Park) making it great alternatives for tenants looking for more cost-effective solutions.

Sydney’s legal district is gradually shifting away from the traditional court precinct as leading law firms relocate to the newly revamped AMP Building at 33 Alfred Street in Circular Quay. This emerging hub will prominently feature Allens, occupying the top nine floors, alongside other major firms such as Lander & Rogers, Maddocks and Pinsent Masons. The movement reflects a broader trend of law firms seeking to upgrade their office space to strengthen corporate image, attract and retain talent, and support a return to in-office work. Recent relocations of Johnson Winter Slattery and Corrs to Quay Quarter Tower, and Gadens to Chifley Square, underline a clear preference for premium, well-located offices that combine prestige, amenity and transport connectivity.

A recent Tenant CS study of 75 mid- and top-tier law firms in Sydney found that around 39% had downsized, 60% had upsized, and the average tenure in a single building was approximately 7.5 years, driven by high relocation and fitout costs. For legal occupiers, these long commitments place a premium on getting building quality, flexibility and location right at the outset, as today’s decisions will frame workplace and brand outcomes over much of the next decade.

Sustainability is now a core filter for office occupiers, particularly larger corporates with formal decarbonisation targets. Tenant CS Director Hamish Mackay notes that for many local and offshore tenants, strong ESG credentials are treated as a baseline requirement, not a “nice to have”

Tenants are gravitating towards higher-grade assets with strong Green Star, NABERS and/or WELL ratings. At the same time, recent analysis indicates only around 28% of Australian office buildings are on track to meet major tenants’ climate needs, highlighting how limited the pool of genuinely future-proof assets still is. This is widening the gap between newly built or comprehensively refurbished towers and older, more carbon-intensive stock.

The future Atlassian HQ at Tech Central (due 2027) illustrates where demand is heading: a low-carbon, hybrid-timber, fully electric building targeting leading sustainability ratings. For tech and innovation-led occupiers, assets of this type align leasing decisions with climate commitments and employee expectations, while reducing exposure to future regulatory and carbon-cost risk.

Melbourne CBD vacancy remains elevated at 17.9% as at Q2 2025. By grade, vacancy is 16.4% in Premium, 19.3% in A Grade and 18.9% in B Grade, keeping conditions firmly in tenants’ favour. At a precinct level, the Eastern Core (13.8%) and North Eastern (13.0%) are the tightest sub-markets, while Spencer (21.9%) and Flagstaff (20.6%) continue to show the deepest vacancy and therefore the strongest leverage for occupiers open to western CBD locations.

Q3 saw completion of the 85 Spring Street refurbishment (~12,000 sqm, ~80% pre-committed), the first major delivery of 2025. This adds a modest amount of prime space and triggers further backfill as tenants upgrade from older buildings. The next substantial wave of new stock is now concentrated in 2026, with the scheduled completion of 17 Bennetts Lane (~12,000 sqm), 7–23 Spencer Street (~46,000 sqm, <10% pre-committed), 51 Flinders Lane (~29,000 sqm, largely pre-committed to WPP), 435 Bourke Street (60,000+ sqm, ~26% pre-committed to CBA) and Town Hall Place (~17,000 sqm, majority pre-committed).

With vacancy still elevated, leasing conditions are likely to remain favourable for tenants over the long term, especially for larger occupiers and those open to secondary locations or backfill space.

In Q3 2025, Melbourne CBD face rents moved higher again across all grades, while incentives remained elevated. Premium net face rents rose 5.9% QoQ to $917/sqm, A Grade increased 5.2% to $764/sqm, and B Grade lifted 0.7% to $606/sqm. On a year-on-year basis, Premium and A Grade face rents are now up 12.5% and 6.4% respectively, while B Grade is 3.8% lower than a year ago.

The impact on effective rent is more muted. Premium effective rents increased 5.9% QoQ to $488/sqm, A Grade rose 5.1% QoQ to $389/sqm and B Grade edged up 0.7% QoQ to $309/sqm, still around 3.4% below Q3 2024. Incentives remain high at around 46.8% in Premium and 49% in A and B Grade, with only B Grade changing this quarter (-0.6%)

The longer-term picture is that face rents have grown, but effective rents have more muted growth. Since 2018, Premium effective rents have slipped from $495/sqm to $488/sqm, A Grade from $405/sqm to $389/sqm and B Grade from $320/sqm to $309/sqm, despite steady headline rent growth. For tenants, leasing conditions remain favourable: high incentives and elevated vacancy continue to contain net effective rents, particularly in A and B Grade stock, where there is still good scope to secure competitive packages on both new and renewal deals.

Melbourne CBD sublease vacancy is now sitting at around 1.2% of stock (62,143 sqm), down from about 1.6% a year earlier and below its long-term average. Most precincts are now under 2%, with the North Eastern precinct still recording the highest level of sublease space.

Despite the decline, Melbourne still records the highest sublease availability of any Australian capital. For tenants, subleasing remains attractive given its lower effective rents, fitted layouts, and shorter terms, offering cost and flexibility advantages over direct lease options.

Melbourne CBD recorded its first period of positive net absorption since 2022, standing at +1,446 sqm in H1 2025. Growth was led by Grade B and Premium, partly offset by continued weakness in A Grade. At a precinct level, the Eastern Core and Western Core outperformed, while Docklands and the North Eastern precinct recorded further negative absorption.

Although the headline shift into positive territory signals a marginal improvement, demand remains well below historical norms. Elevated vacancy and generous incentives ensure occupiers continue to hold strong negotiating power.

Some of the commitments which will shape the future of the Melbourne CBD include:

Our observation of stronger B Grade take-up has been confirmed in H1 2025 with PCA’s biannual report released in August. Melbourne CBD recorded overall net absorption of +1,446 sqm, with Grade B contributing +15,031 sqm, the standout performer across all grades. This uplift reflects tenants relocating from suburban and fringe markets into more central locations, suggesting that for many occupiers, CBD positioning is taking precedence over building quality.

This contrasts with other capitals where the “flight to quality” has dominated. In Melbourne, Premium absorption was positive but more modest (+4,520 sqm), while A Grade contracted. The data indicates tenants are prioritising affordability and location over quality upgrades, softening the flight-to-quality narrative in this market.

From 1 January 2026, the Melbourne congestion levy on off-street parking will rise sharply, with Category 1 (CBD) increasing from $1,750 to $3,030 per bay per year and Category 2 (inner fringe) rising from $1,240 to $2,150 per bay per year – lifts of roughly 70%. The Category 2 levy area will also expand to include parts of Burnley, Cremorne, Richmond, Abbotsford, South Yarra, Windsor and Prahran, as well as sections along St Kilda Road, while the Queen Victoria Market area moves to the lower Category 2 rate.

The impact will be most pronounced for tenants with large parking allocations, where the levy is typically passed through via outgoings or licence fees and can materially increase total occupancy costs even if office rents remain steady. Several fringe and city-edge precincts that were previously relatively low-cost for parking will now carry a much higher levy. As a result, the congestion levy will become a more important factor for companies with high parking requirements when assessing which suburbs and buildings to target in the next lease cycle, sitting alongside rent, incentives, transport access and staff catchments in occupier decision-making.

Fitted space continues to be leased ahead of vacant space, but in the sub-300sqm market there is now a clearer hierarchy emerging. Well-designed, modern spec suites are being leased noticeably faster than older or more generic specs, as smaller tenants prioritise quality, convenience and avoiding upfront fitout spend. Older spec fitouts are still leasing, but typically require sharper incentives or some landlord contribution towards refresh works to compete with newer, better-presented options.

In Melbourne, ESG credentials remain an important consideration, with tenants continuing to prefer buildings that offer strong NABERS ratings and sustainability initiatives. However, these buildings typically sit in the Premium and A Grade market, where demand has weakened. A Grade recorded the largest contraction in H1 2025, while B Grade was the only segment to show meaningful positive absorption. This pattern highlights that for many occupiers, affordability and location are outweighing ESG aspirations. Cost-conscious tenants are gravitating toward B Grade stock, even as premium assets hold their environmental advantage. With face and effective rents in secondary stock under pressure, cost remains the dominant driver of leasing decisions, while ESG is increasingly seen as a “nice to have” rather than a “must have”.

Brisbane CBD vacancy remains at 10.7%, consistent with the latest PCA bi-annual report. Premium vacancy is unchanged at 3.8%, while A Grade and B Grade also hold at 9.6% and 14.9%, reinforcing the continued split between tight Premium availability and softer mid-tier conditions.

On the supply side, 205 North Quay is now complete and fully occupied by Services Australia, with 360 Queen Street (~45,000 sqm) set to be the next major addition. The tower is due in late 2025 and is now close to 90% pre-committed, led by BDO, Herbert Smith Freehills and other large occupiers. Beyond this, committed future supply remains limited, with the 450 Queen Street refurbishment (~17,500 sqm, 2026) and Waterfront Brisbane North Tower (~72,000 sqm, 2028, ~50% pre-committed) forming the next wave of new stock. Other mooted projects, including 101 Albert Street and 60 Queen Street, remain uncommitted and are unlikely to reach the market before 2028.

With Premium vacancy already tight and limited new space coming online, competition for high-quality buildings remains elevated. In contrast, A and B Grade vacancy is stable but high, offering tenants broader choice, stronger incentives and greater negotiation leverage in the mid-tier.

Gross face rents increased again in Q3 2025, with Premium rising to $1,256/sqm, A Grade to $984/sqm, and B Grade to $810/sqm. Growth was strongest in A Grade (5.0% QoQ), followed by Premium (3.7%) and B Grade (2.5%). On an annual basis, rents have lifted between 11–14%, reflecting ongoing upward pressure despite mixed demand conditions.

Incentives edged lower across all grades, now sitting at 33% in Premium, 34.5% in A Grade, and 38.5% in B Grade. The reduction is modest but continues the trend of tightening terms in higher-quality assets as Premium supply remains constrained and stronger A Grade options absorb enquiry.

These movements pushed effective rents higher again this quarter. Premium rose 5.3% QoQ, A Grade lifted 6.6%, and B Grade increased 4.2%. The strongest momentum remains in A Grade, where falling incentives are amplifying rental growth despite vacancy holding at 9.6%. B Grade continues to offer the most favourable terms for tenants, with incentives near 40% softening the impact of rising face rents.

Brisbane CBD sublease vacancy was recorded at 0.9% of total stock (~20,900 sqm) in July 2025, down from 1.2% (~27,800 sqm) in January. This places current sublease availability below the city’s long-term average of ~1.0%. Reductions of sublease vacancy can be attributed to the removal of listings, transfer of sublease to direct vacancies and uptake of the space.

Leasing activity in the Brisbane CBD remained subdued in Q2 2025, with many occupiers opting to renew rather than relocate amid cost pressures and ongoing caution. Decision-making timelines remain extended, particularly for larger corporates, contributing to a slow flow of new commitments.

Despite this softer backdrop, Brisbane recorded the strongest net absorption of any CBD in the first half of 2025, reflecting a handful of large occupier moves rather than broad-based demand. This strength was concentrated in Premium assets as we noted vacancy tightened to 3.8%

Notable tenant movements in Q3 2025 shaping Brisbane CBD include:

Brisbane now ranks as the most expensive city to build in Australia, with average construction costs hitting approximately $5,009 psqm, edging ahead of Sydney and Melbourne. Pressure is mounting: Arcadis reports a 5.2% cost escalation in 2024, with a further 5% projected for 2025, and a staggering 30.5% cumulative cost rise expected by 2029, driven by Olympic-related demand, acute labour shortages, and wage inflation. The labour market is stretched estimates suggest a shortfall of 41,000 skilled workers across Queensland, exacerbating delays and escalating budgets.

At the same time, government infrastructure programs (notably 2032 Games preparations and Cross River Rail) are siphoning off capacity and labour from commercial projects, further squeezing new office developments. Adding to these pressures is poor labour productivity on major projects. Industry leaders warn that union-backed rostering is leaving some sites effectively operating at only two to three productive days per week, even as wages climb. Treasury modelling suggests this could lift project costs by up to 25% by 2030, highlighting systemic inefficiencies that make new office towers harder and slower to deliver. These conditions are a double-edged sword, on one hand, the difficulty and cost of delivering new high-quality towers gives landlords reason to hold firm on pre-commitment pricing and tighten incentives. On the other, there’s growing opportunity in existing A and B Grade buildings, where owners are investing in sustainability and productivity upgrades to remain competitive and leveraging incentives to attract occupiers.

Brisbane’s flight-to-quality continues to accelerate as organisations compete for talent and reinforce in-office attendance. With only eight Premium buildings in the entire CBD, high-quality space is structurally scarce, and demand is concentrating heavily at the top end of the market. In Q2 2025, Premium vacancy fell sharply from 7.3% to just 3.8%, its lowest level in more than four years, underscoring how quickly new or refurbished space is absorbed once it becomes available. By contrast, vacancy increased in A Grade (to 9.6%) and B Grade (to 14.9%) as occupiers either traded up or sought better amenity without paying Premium rents. The divergence shows that while overall CBD vacancy edged up to 10.7%, genuine high-quality options are shrinking. For tenants targeting Premium towers, early engagement is becoming essential. Those prepared to consider upgraded A or B Grade assets will benefit from broader choice, stronger incentives, and materially better negotiating leverage.

New CBD towers are thin on the ground over the next few years, with only a small number of committed projects adding to the total office pool and much of that space already pre-leased. From here, most leasing options will come from churn and backfill as tenants move into new or refurbished buildings, rather than from large volumes of brand-new stock. At the same time, some older secondary assets are being withdrawn or converted to other uses, meaning the market is gradually reshaping more than expanding. For tenants, the practical outcome is a market where the best value is increasingly found in existing A and better B Grade buildings, particularly refurbished or partially upgraded assets - offering a mix of established locations, improved services and negotiable commercial terms.

Brisbane’s fringe office market is heating up as more businesses look beyond the CBD for workspace. With rising rents and tighter availability in the city centre, companies are increasingly turning to fringe areas like Fortitude Valley, South Brisbane, and Newstead for more affordable, high-quality office spaces. According to the PCA, the fringe recorded a 10.5% vacancy, which has been on the decline for a number of years.

This shift is being driven by vacancy rates tightening and limited new supply, Brisbane’s fringe office market is proving to be an attractive alternative for companies looking to expand or relocate.

In most Australian cities it’s a tenant’s market and will be for the foreseeable future. Landlords are competing to secure quality occupants on long leases and are more flexible than they have been in years.

Opportunistic tenants are taking advantage of favourable market conditions by renegotiating terms in their existing space or relocating to a better building.

To secure the best terms, tenants need only find the soft spots in the market and develop their strategy around landlord motivators.

But the landscape is challenging to navigate alone. Even in a favourable market, there's more to negotiate, and tenants need access to the whole market to get the best deal.

Tenant CS is an independent tenant advisory firm that exclusively represents tenants in commercial negotiations to secure favourable lease terms and savings.

Book a discovery call to find out how we can help you with your next lease negotiation or relocation project.

We acknowledge the Traditional Custodians of the lands on which we work. Our offices are located on the land of the Gadigal peoples of the Eora Nation and the Wurundjeri peoples of the Kulin Nation. We acknowledge their continued connection and contribution to land, water and community, and pay our respects to Elders past and present.

We’re proud to be an inclusive workplace, where diversity in all its forms are valued and every member of our team is encouraged to bring their whole self to work.

.gif)